Unlike other types of trusts often used in estate planning, the primary goal of a special needs trust is to provide for the needs of an individual who is disabled throughout his or her life.

Federal and state benefits are generally available to qualifying children and adults who have special needs. If your child qualifies for government benefits, one of your goals may be to help make sure that his or her eligibility continues into the future. A special needs trust can help you attain this goal. In addition, this type of trust can provide for supplementary care and services for your loved one.

Medicaid, a joint federal-state program, provides medical assistance to those who are disabled and can demonstrate financial need. Children and adults can qualify for Medicaid only if their monthly income and the value of their other assets fall below certain limits, which vary from state to state. Most states set a $2,000 asset limit.

In determining eligibility for Medicaid, a state may count only the income and assets that are legally available to the applicant. A special needs trust restricts the beneficiary’s own direct access to the assets in the trust to such an extent that the assets are not considered legally available to the beneficiary. Thus, a special needs trust can protect Medicaid eligibility because assets in the trust are uncountable.

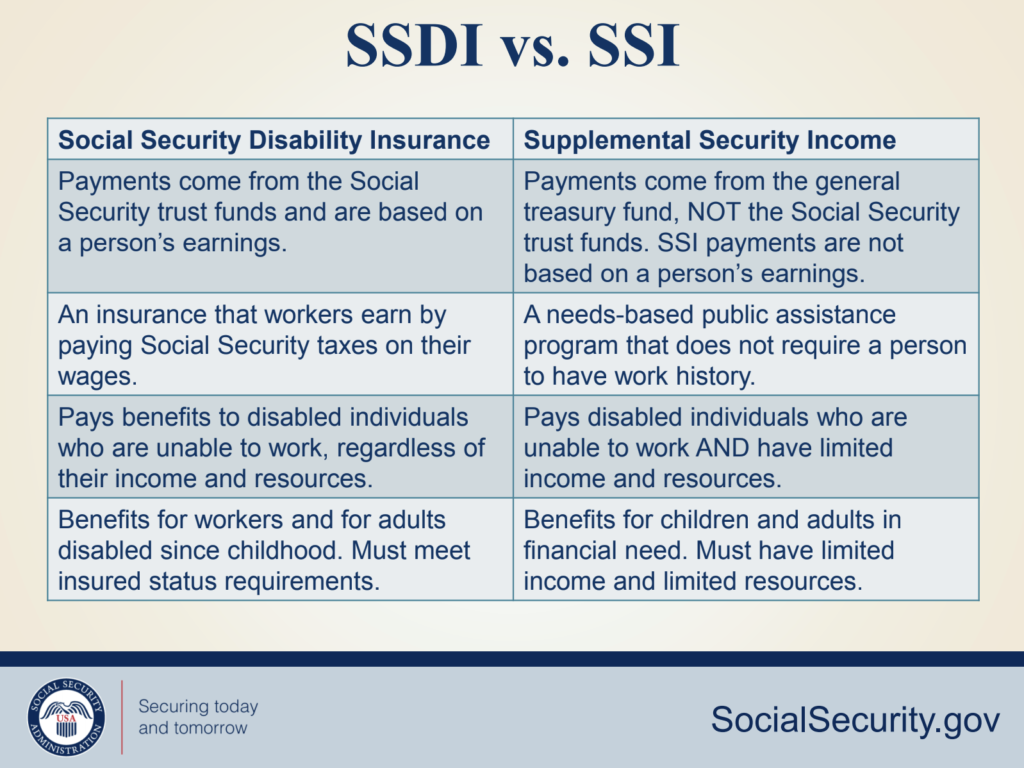

Children and adults with special needs who have limited income and resources often receive monthly benefits from Supplemental Security Income (SSI). These cash benefits can be used for basic needs such as housing and food. But because SSI benefits are need-based, inheriting money can mean that a child with special needs will lose eligibility for this benefit program. By naming a special needs trust as your beneficiary instead of your child, however, assets can be devoted to the care of your loved one. In addition, since SSI recipients are normally automatically eligible for Medicaid benefits, preserving your child’s eligibility for SSI may preserve their eligibility for Medicaid as well.

A special needs trust can be especially useful if you want to provide care and services necessary for your child’s well-being, without supplanting Medicaid benefits.

Although Medicaid pays for a number of medical costs, including hospital bills, physician services, and long-term care, it will not subsidize items and services considered nonessential. These may include health-related expenses such as eyeglasses, dental care, rehabilitation services, and home health aide services, as well as personal expenses such as transportation, computer equipment, and vacations.

To help confirm that trust assets are not considered legally available to the beneficiary, the trustee must have sole discretion over the distribution of trust income and principal. The beneficiary must have no control over the trust and no right to demand distributions from the trust. The trustee should purchase goods and services directly on the beneficiary’s behalf, instead of giving the beneficiary money from the trust to purchase items needed.

Although there are many types of special needs trusts, they fall into two general categories: the third-party special needs trust, which is funded with assets belonging to someone other than the beneficiary; and the self-settled trust, which is funded with assets belonging to the beneficiary.

A trustee is a person or institution selected to administer a trust and manage its assets. The trustee’s role is to adhere to the terms of the trust document and fulfill its objectives. You may wish to name yourself or another family member as trustee of the special needs trust, or you may wish to name a professional trustee. Another option is to name a family member and a professional trustee as co-trustees.

If you set up a special needs trust through your will, you might also want to draft a letter of intent to describe how you want your child to be cared for after you’re gone.

Although it’s not a legal document, it can provide important information to guardians, trustees, family members, and others involved in the care of your child. The letter may address such issues as your child’s medical needs, daily routine, interests, likes and dislikes, religious practices, living arrangements, social activities, behavior management, and degree of self-sufficiency. Such a letter can prove invaluable to your child’s caregivers and can also make the transition to a new living situation as smooth as possible for your child.

Explain to siblings or other family members why you’re setting up the special needs trust. Although siblings might expect to receive equal inheritances, more resources will probably need to be set aside for the benefit of your child with special needs. Explanations and clear directions now may help avoid family conflicts later.

I am a Special Needs Trust Attorney and I am here to help. I am the founder of a nonprofit corporation to that provides quality information about resources available to families as well as providing affordable Special Needs Trusts and estate planning for families. I have over 20 years of experience helping families just like yours. Find out more information at SpecialNeedsTrustsOnline.com or click here to set up a free appointment.

I am a Special Needs Trust Attorney and I am here to help. I am the founder of a nonprofit corporation to that provides quality information about resources available to families as well as providing affordable Special Needs Trusts and estate planning for families. I have over 20 years of experience helping families just like yours. Find out more information at SpecialNeedsTrustsOnline.com or click here to set up a free appointment.

I am Tom Sannicandro, a

I am Tom Sannicandro, a

Let relatives know you have created a Special Needs Trust for your child with a disability. This is to be sure if Grandma or Grandpa or Aunts and Uncles, etc. plan on leaving money to your child with a disability in their will, let them know they should leave the portion for the child with a disability to the Special Needs Trust. “to the trustee under The ‘your child with a disability’s name’ Trust for the benefit of your child with a disability’s name’.”

Let relatives know you have created a Special Needs Trust for your child with a disability. This is to be sure if Grandma or Grandpa or Aunts and Uncles, etc. plan on leaving money to your child with a disability in their will, let them know they should leave the portion for the child with a disability to the Special Needs Trust. “to the trustee under The ‘your child with a disability’s name’ Trust for the benefit of your child with a disability’s name’.”

The trust is intended to help preserve funds for a person with a disability, and enhance the person’s quality of life while protecting his or her eligibility for public benefits, such as Medicaid and Supplemental Security Income (also known as “SSI”).

The trust is intended to help preserve funds for a person with a disability, and enhance the person’s quality of life while protecting his or her eligibility for public benefits, such as Medicaid and Supplemental Security Income (also known as “SSI”).